Has the VC Industry Learned From its Mistakes?

Has the VC Industry Learned From its Mistakes?

The impending IPOs of several notable VC-backed companies signal early signs of a rebound for the industry after a critical low point. If the worst days are truly behind it, will anything change?

Chip-maker Arm IPO’d on Thursday to a broadly supportive public market, and Instacart is expected to follow suit later this month. That may or may not mean anything to you, but it was a notable event in the business community for a few reasons.

For one, it was the largest IPO of 2023, in year when IPOs have been down 40% compared to last year and nearly 90% compared to 2021. This a good sign for the market as a whole, which has been in somewhat of a limbo since the Federal Reserve began raising rates in March 2022 to combat rising inflation. But it’s a particularly promising sign for the private markets, which have, by and large, fared much worse than the public markets in this higher interest rate environment. The private markets, including the venture capital industry, rely, in part, on public market sentiment as a guidepost when evaluating its own deals. If Arm succeeds as a publicly listed company, it’s a good sign for the VC community.

But Arm’s IPO is also notable because of the company’s owner, a Japanese investment firm called SoftBank. In 2017, SoftBank and its CEO, Masayoshi “Masa” Son, founded the Vision Fund—the world’s largest “tech-focused” venture capital fund with over $150 billion in assets under management. With all the money in the world, SoftBank and Masa proceeded to quickly rise to quasi-celebrity status by aggressively funding companies that Masa personally perceived to be the next disruptive billion-dollar companies, often based on nothing more than his instinctual gut feeling. More on this later, but suffice it to say that, after having just posted a $32 billion loss in this last fiscal year, SoftBank could use a win here with Arm’s IPO.

If Arm’s IPO is indeed the first early signal of a sea change in the currently murky venture capital waters, then the inflection point serves as a good opportunity to assess the state of the industry—what’s gone wrong, what’s gone right, and what, if anything, will change going forward.

At a high level, the basic way the venture capital industry works is:

A VC firm goes out and raises money for their fund, typically from institutional investors like endowments, family offices, and pension funds, but also sometimes from individuals. These outside investors in the VC fund are called “limited partners” or “LPs”.

The firm’s investors spend time sourcing potential deals (i.e. finding startups to invest in) through a whole host of channels. They meet with founders, they attend events, they keep up with the latest industry news, they talk to their peers and keep track of who’s investing in what, they read through the cold emails they’ve received from hungry founders while on the toilet or waiting in line for Sweetgreen, and so on.

The firm starts to narrow down its pool of potential investments until it finally arrives at a shortlist of companies that it’s willing to put in additional time and resources to dive deeper on. The process of digging into a company is known as “due diligence.” At the VC stage, diligence could involve anything from contacting the founder’s references or former colleagues, to reaching out to the company’s vendors or customers (if any), and, of course, reviewing any company contracts and financials. But, because early-stage investing is necessarily, well, early stage, often companies will have little or no financials or meaningful contracts to go off of. Plus, even if the company does have financials, it’s usually so early in the game that any projections often aren’t worth the paper they’re printed on. So, the investor does the best she can with as much information she can collect under the circumstances to make the best decision possible in a finite amount of time.

Once the VC has invested its LPs’ money, typically by taking equity in a nascent but promising company, the VC will repeat the process with other standout startups in an effort to maximize its chances at a big return. Because VC firms are investing at such early stages in a company’s life cycle, they live and die by what’s known as the “power law”: the vast majority of the returns come from a disproportionately small number of companies in the VC’s portfolio. In other words, if the VC invests in ten companies, eight may fail, while two may generate enough returns to make the VC and its LPs money.

The firm will sometimes help shepherd its portfolio companies along as they (hopefully) grow and take on more funding. But, depending on how it operates, the VC could also invest its money and proceed to do absolutely nothing, hoping at least one or two of its bets catch fire. Regardless of approach, if one of the VC’s companies in fact continues to grow and raise more money, the company will be worth more. Eventually, if all goes to plan, that company will go public or be sold to one of the very Silicon Valley behemoths that the original founder loathed enough to forego working for in order to start a company in the first place, upon which time the investors and founder will have the opportunity to cash out and receive a big pay day, with everyone going home happy.

This is, in many ways, an oversimplification of the process, but you get the point. At its core, the job of a VC is to take a pool of money and use the VC’s time, skill, and expertise to make early and educated bets on people, ideas, and businesses, in the hopes that a non-trivial number of those bets turns out to be the next Google or Uber.

The last decade saw a massive flight to venture capital (which, by all accounts, remains a small part of the broader private equity industry). This trend culminated in 2021, when the value of venture capital investments in the U.S. amounted to approximately $345 billion, nearly twice as much as the previous year and many multiples of what it was back during the dot-com bubble.

There are plenty of reasons for this movement, but an undeniable force was the low interest rate environment that prevailed for the better part of the last decade. From the investor standpoint, when rates are low, relatively safer options for LPs become less attractive, so LPs have a greater appetite for the riskier VC space. Low rates also make the sort of early-stage, high-growth companies that VCs like to invest more attractive because the prevailing interest rate is a fundamental component in how investors discount future cash flows back to their present value. Those companies, in turn, find it easier to borrow money to fuel their growth, and require a lower return on their corporate finance projects to make the investment of capital worthwhile. It’s a virtuous cycle, at least while rates remain low.

So, up until 2022, when interest rates were at historic lows of near zero, needless to say it was all champagne and cocaine for the VC industry. That all changed when we started to experience a period of persistent and prolonged inflation, which the Federal Reserve sought to tame by systematically raising rates. In the blink of an eye, the industry was relegated to warm beer and vape pens.

During its time of opulence, though, something notable happened within the burgeoning industry. See, when LPs are champing at the bit to give VCs their money, chances are the VCs are going to take it. Not only that, but all that easy money will cause more people to start becoming VCs. Unfortunately, though, the amount of new entrepreneurs who are willing and able to start worthwhile startups simply can’t scale at the same rate. The outcome shouldn’t come as a surprise: too much money was chasing too few investment opportunities.

More noteworthy, though, were the second-order effects of this supply/demand mismatch. See, when money is aplenty for startups, this shifts the power dynamic away from VCs and towards the young companies looking for funding. This means that the latter are more likely to be able to dictate who they take money from, when they take more of it, and how much they take.

So, the state of play up until 2022 was basically that VCs, inundated with more cash than they’ve ever had before, were running around trying to invest in companies who all of a sudden weren’t so desperate for just any VC to fund them. The end result was twofold:

Companies that were desirable got more money than they needed/than they were “worth,” and companies lower down in the desirability stack that shouldn’t have gotten any money at all, got some money. Both of these things caused the growth sector to balloon (or, more aptly, bubble).

VCs, in a rush to meet the timelines of startups seeking to capitalize on the moment, let some of their investing principles and best practices fall by the wayside. Namely, out of fear of missing out on the next hot startup, VCs felt pressure to stop doing so much of that pesky due diligence before investing. If you’re an up-and-coming growth company in 2020 and the venture world is your oyster, why bother with the VC firm that wants to dig in to your business to determine if it’s worth investing in? Just take the easy, no-strings-attached money. This dynamic created a prisoner’s dilemma: if everyone does adequate diligence, then the ecosystem of VCs as a whole is better off; but once firms started investing without doing much, if any, diligence, others had to follow suit in order to stay competitive.

Underlying both of these bad outcomes is a reality of venture investing. Although VCs are incentivized to generate the highest returns they can (because the most significant portion of their fee comes as a percentage of profits) they have little skin in the game when it comes to the investments they make. Most are largely playing with their LPs’ money, and because they’re taking equity in a number of early-stage companies, they’re comfortable with most of those “bets” going to zero, so long as at least one returns the fund. The risks are allocated asymmetrically, so when investing timelines are shortened, many VCs have demonstrated a bias towards cutting corners to invest, rather than missing out on a seemingly great opportunity because it didn’t meet the strictures of its investing timeline and guardrails.

You might read all of this and say, “Who cares?” And sure, at one level, you’d be right. A bunch of capital allocators made risky bets, funded by big and sophisticated institutions who knowingly gave their money to VC firms with the understanding that most of the investments the VC would make wouldn’t pan out, and, surprise, most of their investments didn’t pan out.

Setting aside the fact that LPs are often pension funds who are allocating people’s hard-earned savings, the two points above matter because they helped create, or at the very least exacerbate, the downturn that the VC industry now faces by fueling a significant number of, at best, toxic companies and, at worst, criminal ones. Accordingly, some self-reflection is warranted.

Remember Arm, the SoftBank-owned company going public? Well, a while ago, I wrote about how Sam Bankman-Fried of FTX was a poster child for the “move fast and break things” movement. But if the Notorious SBF was a poster child for MF&BT, then SoftBank is the poster parent. Since 2017, Masa, through the Vision Fund, has had his hands all over nearly every major startup implosion of the last few years.

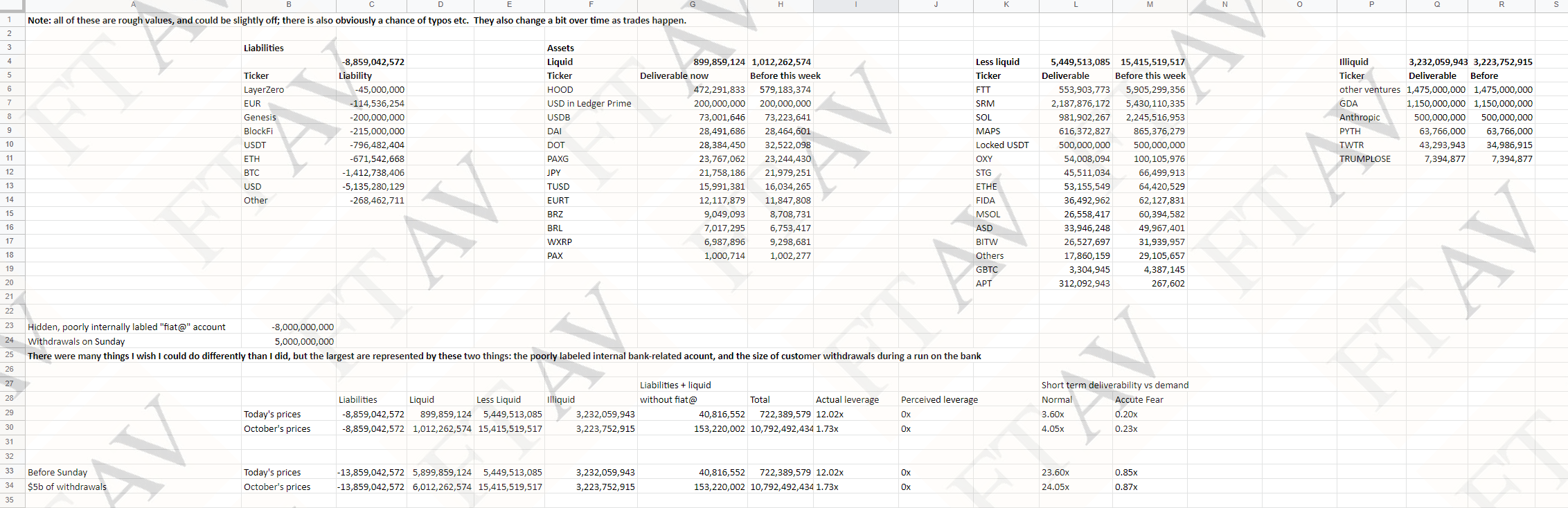

Of course, there was FTX. SoftBank wrote down its $100 million investment in the company to $0 in November 2022, just months after having valued FTX at $32 billion in January of the same year. FTX’s valuation, by the way, was predicated on nothing more substantial than an excel spreadsheet, prepared by Bankman-Fried, that looked like this:

Note that FTX’s biggest asset on that “balance sheet” was $2.2 billion (“dollars”) worth of Serum tokens, which were tokens created and promoted by FTX that the company issued to itself.

Then there was WeWork’s catastrophic implosion. Masa committed to investing $4.4 billion in the real estate “technology” company after just one ~12 min tour with the founder, Adam Neumann, and one subsequent meeting thereafter. By 2019, a month before the company laid off 2,400 employees, SoftBank owned 80% of WeWork.

Clearly, neither the FTX investment nor the WeWork investment screamed principled investing based on robust due diligence. But the list doesn’t end there. There are a host of other, relatively lesser-known frauds and comedies that were propped up Weekend at Bernie’s style by SoftBank and other VCs who failed to do the work to dig in to what they were investing in. There was Zume Pizza, the pizza-making robot delivery truck company that SoftBank invested $375 million in (valuing the company at $2.25 billion despite having brought in less than $1 million in revenue), Zume Pizza, shockingly, shut down earlier this year. Then there was IRL, a social media site that SoftBank invested $150 million in, which was forced to shut down after its user-base turned out to be 95% bots. Or what about Oyo, basically the WeWork of hotels, which SoftBank has sunk $2 billion into. Despite the implosion of WeWork, Oyo’s business model and its “charismatic” 25-year-old founder are largely carbon copies of WeWork and Neumann (down to the fact that it hemorrhages cash and has been struggling to go public). Oyo, once valued by SoftBank at $10 billion, has been written down by almost 75%. The list goes on…

The point here is that, if VCs (justifiably) want to claim that successful investments in multiple home-run startups is more skill than luck, then repeated investments in a string of borderline dysfunctional money-losing companies and/or frauds can’t be chalked up to the investing gods. Rather, it’s the product of a systemic failure on the part of investors to take their time to diligence companies and resist the temptation to pour LPs’ money into the next shiny startup just because their peers do.

As one prominent early stage investor said of the recent bubble:

[O]ne of [the] key pieces of discipline [of a venture capitalist] is asking uncomfortable questions and doing uncomfortable diligence and, you can trust people, but you need to verify, that is a key part of the job. You can trust the founders, but you have to verify that the data you have is correct. I [was doing] diligence, asking for very basic stuff [like] your bank statements, your P&L […] and had many founders say to me you're asking for more diligence than the lead [investor]… Like people did not want to do this stuff.

During this period [of peak VC activity], founders used the hot market to not participate in the due diligence process… a lot of times people suspend[ed] disbelief.

To be sure, diligencing early-stage companies is no easy task. It’s a lot easier to diligence a company with a product or service track record and trailing revenues and free cash flows than it is a startup that may be pre-revenue and almost certainly pre-profitability. But reviewing non-GAAP financials, talking to customers and references, and analyzing company-specific KPIs can, and has, been done for decades. The recent trend of failing to do it was simply a malady of laziness and greed.

SoftBank is also far from the only culprit here. A large portion of the industry is to blame, including the mega-successful firm Sequoia, which backed the likes of FTX to the tune of $200 million and whose lead partner on that deal, Alfred Lin, recently went on a not-so-sorry apology tour to explain how he didn’t know what else he and Sequoia could have done to avoid the FTX calamity and wasn’t sure if he could have “spotted any tells.” (In response to which I would refer Alfred to the above FTX “balance sheet.”)

But all the more proof that early-stage investing can be done the right way are all of the dogs that didn’t bark. For every VC that funded an FTX or IRL, there were countless others who didn’t. Without naming names, Josh Kushner of Thrive Capital recently said that, despite watching his peers make “money hand over first” during the crypto craze, his firm’s “discipline[d]” approach to the crypto industry led Thrive to conclude that most of the hot crypto companies at the time were largely “solutions in search of problems.” Then there’s Dragonfly Capital’s Alex Pack, who, in 2018, saw obvious “red flags” with FTX during his diligence process that indicated Bankman-Fried’s “risk-taking was catastrophic.”

So, as Arm takes on the public markets with initial signs of public support, the lingering question for the VC community as it starts to pick up steam again will be whether the industry will have learned anything from its mistakes of the past few years. Fundamentally, VC investing is about people—it’s about investors giving money to founders to build businesses for customers. And that’s a great thing. As Alfred Lin of Sequoia says, VC is “a trust business. And yes, we need to trust and verify, and we try to verify what we can. But we start from a position of trust, because if we don’t trust the founders that we work with, why would you ever invest in them?” That may be true, but the last few years have shown that if you don’t also do the verify part, then chances are you’re burning your LPs’ money. Here’s hoping that patience and principles make a comeback in this new era of VC investing so that we can all witness a lot more Xs (the company formerly known as Twitter) and a lot less FTXs.

Good write up 💯